November 14, 2024

Introduction

On the outskirts of a small town in Western Cornwall, England, is a dairy farm. It’s a remote area, surrounded on three sides by the sea and almost 300 miles from London. When the winter storms roll in it can feel like it’s the end of the known world. The farm has been in the family for 7 generations and has slowly grown in scale.

From 20 cows milked by hand in the 1950s, it had grown to 100 cows milked in a new herringbone parlour by the 1980s.

Today the herd numbers more than 200. In the past few years, the farm has invested heavily in a new robotic milking system. The cows each wear a necklace which transmits their details to one of three milking robots. They choose when they would like to be milked. Their tailored feed is dispensed while the milking system attaches automatically to their udder, which has been individually mapped.

Away from the milking robots, a further two “poo-bots” hoover up the manure and pump it into the slurry pit. Another robot dispenses further feed to the cows as and when needed. Data from the whole operation is sent to the farmer in real-time through a mobile app. And everything is powered by more than 100 solar panels which sit on the roof of the cowshed.

The cows are happier – milk yields are up. But why get energy from the sun and spray the slurry on the fields, rather than use the slurry for energy and buy in fertiliser? Cows poo all the time, but the sun doesn’t always shine in the UK.

Why was biogas not a viable option for a remote, moderate-sized UK farming business?

Let’s look at another farming business, this time in Brazil.

Cocal is a sugarcane grower and processor. They’ve been active for more than 40 years, manage 142k ha of land and grow 8.7million tonnes of sugarcane a year. This is then processed at two facilities in Paraguaçu Paulista and Narandiba, both in Sao Paulo state.

Their cane is used to make a full spectrum of energy products: sugar, ethanol, electricity, green carbon dioxide and biogas, which is then upgraded to biomethane.

Their first biogas plant, at the Narandiba facility, houses the country’s first independent biomethane distribution grid system, supplying biomethane to GasBrasiliano. This plant has an installed capacity of 5 MW of electrical energy and produces 8million cbm of biogas annually from sugarcane by-products vinasse, filter cake, and sugarcane waste.

Their latest plant at Paraguaçu Paulista focuses entirely on biomethane production, incorporating lessons learned from the Narandiba facility to enhance efficiency. Additionally, the plant is benefiting from Brazil’s RenovaBio program, with the aim of being certified for the commercialisation of carbon credits (CBIOs). The green and circular economy model implemented in Narandiba will also be applied at Paraguaçu Paulista.

One financial and environmental benefit is following biogas production, the materials used in the process will be returned to the fields as biofertiliser, enriching the soil and advancing sustainable practices in Brazil’s sugarcane farming.

So why has biogas been viable in Brazil in the sugarcane sector, but not in the UK in the dairy sector?

This report aims to help answer this question, and in doing so it might help you decide whether biogas is also the correct answer for your business.

2. Benefits of Biogas

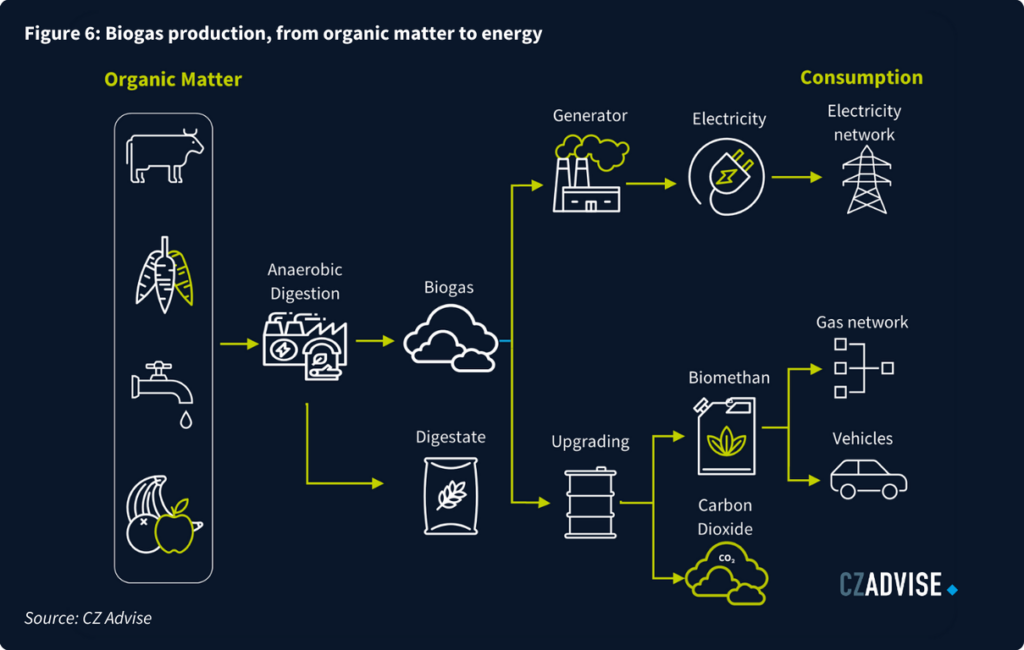

Biogas is mainly comprised of methane and carbon dioxide, made by anaerobic digestion of organic matter. Biogas (or upgraded biomethane) can be combusted for energy/electricity in much the same way that natural gas can, and so turns waste into renewable energy.

It therefore has a hint of alchemy to it: the promise of turning base metals into gold. Unfortunately, like most alchemy it also has a hint of distaste to it: the raw materials here are agricultural waste, sewage and slurry.

Anaerobic digestion therefore has two benefits:

- Firstly, it provides useful waste treatment.

- Secondly, the resulting biogas or biomethane can decarbonise energy demand.

Biogas and biomethane are also flexible energy sources:

- They are omnivorous: they can be made from many different waste feedstocks.

- They can be used to make heat and/or power for industry, agriculture, homes and transport, and so can decarbonise multiple sectors.

This flexibility is valuable as it allows countries to evolve how they transition to a low carbon economy and help to decarbonise hard-to-abate sectors.

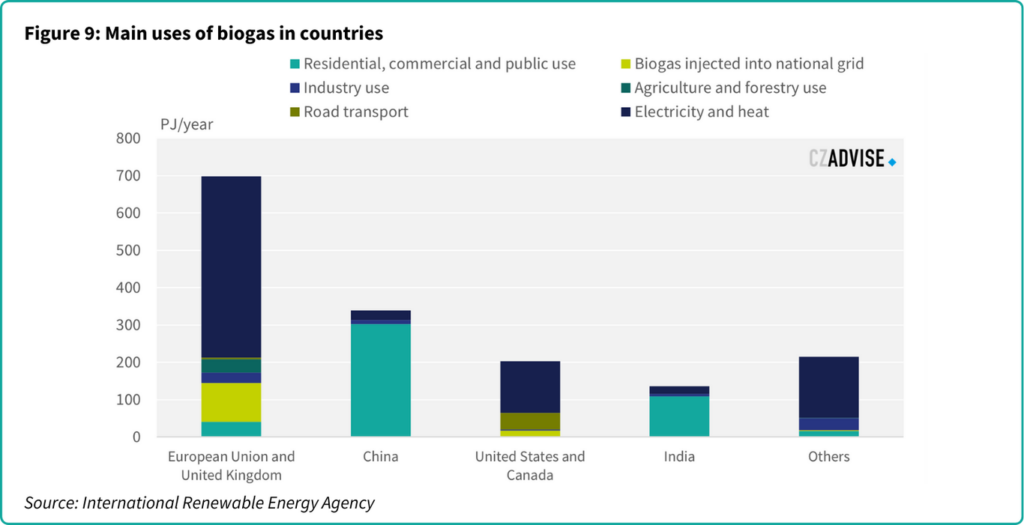

3. Biogas in Europe

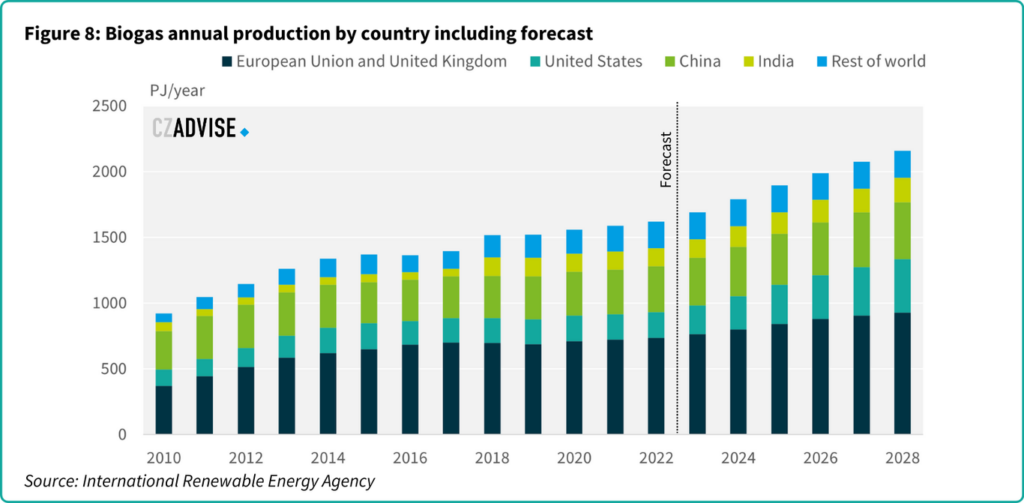

Europe is the world leader in biogas, accounting for nearly half of the world’s production. Its dual benefit in reducing waste and generating low-carbon power means that it’s been incentivised by governments across the continent as Europe seeks to reduce its carbon emissions to net zero by 2050.

Its roll out has been supported by the European Union’s Renewable Energy Directive. This sets a target for renewable energy to account for 42.5% of overall energy consumption by 2030. Member states are allowed to provide support for renewable energy schemes, subject to some conditions. As a result, one study found that by the end of 2017, almost 150 measures had been put into place across the EU to promote biogas, of which more than two-thirds were financial support. These measures include:

- Electricity feed-in tariffs,

- Feed-in premiums,

- Support to integrate biogas generators into the gas grid,

- Simplified processes for approving the construction of digesters and biogas plants,

- Tax exemptions.

As a result, Europe currently has around 20,000 biogas plants and 1,400 biomethane plants.

4. Focus on the UK

In the UK, support for biogas initially came through the renewable heat incentive. This offered a fixed income for generation of heat from renewable energy sources. Small-scale electricity generators also benefitted from feed-in tariffs for power made from low-carbon sources. But only anaerobic digesters with a capacity of less than 5MW were eligible.

Larger scale projects instead received Renewables Obligation Certificates for their power. These could then be sold to other electricity producers who generated using higher carbon methods. This was subsequently replaced by a Contracts for Difference scheme.

Government support in recent years has shifted from anaerobic digestion to make biogas towards biomethane. Currently, the government offers 15-year tariff support for biomethane which is injected into the gas grid. However, this scheme is only open to new anaerobic digestion plants and not for the conversion of existing biogas projects into biomethane.

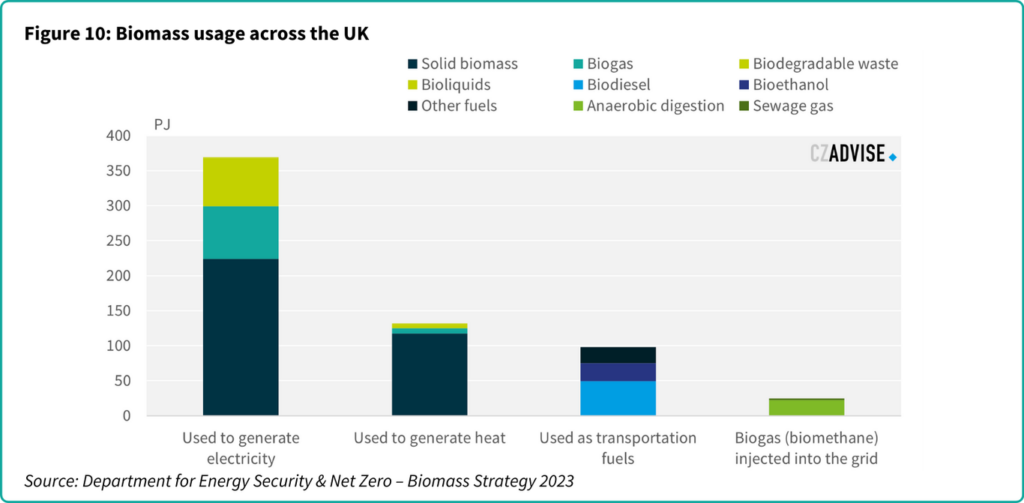

Figure 11: Detailed view of biogas usage across the UK

| Usage | Source | PetaJoules (PJ) |

| Used to generate electricity | Solid biomass (plant and animal) | 223.9 |

| Biogas (landfill, sewage and anaerobic digestion) | 75.6 | |

| Biodegradable waste | 68.4 | |

| Bioliquids | 1 | |

| Used to generate heat | Solid biomass (wood, waste wood, plant and animal biomass) | 117.7 |

| Biogas (landfill, sewage, and anaerobic digestion) | 7.6 | |

| Biodegradable waste | 5 | |

| Bioliquids | 1.8 | |

| Used as transportation fuels | Biodiesel | 49.3 |

| Bioethanol | 25.9 | |

| Other fuels (eg. Biomethane, hydrogenated vegetable oil (HVO), sustainable aviation fuel (SAF), drop-in fuels) | 23 | |

| Biogas (biomethane) injected into the grid | Anaerobic digestion | 22.3 |

| Sewage gas | 2.2 | |

| Total | 623.7 | |

Looking across recent years, the UK’s support has clearly been successful. There are now more than 700 anaerobic digester plants in the UK, of which more than 100 produce biomethane for injection into the national gas grid. In 2022 around 6.2TWh of biomethane was made by anaerobic digestion. The government’s biomass strategy envisages that this will rise to at least 30TWh by 2050.

However, we worry that the pace of uptake of anaerobic digestion to make biomethane may slow. There are several barriers the UK needs to overcome.

4.1 Cost

Anaerobic digesters are expensive. They have significant upfront capital expenditure and ongoing operating expenditure. The UK government estimates that a 6 MW biogas plant – a medium sized biogas plant – costs £17million (USD 22million) to build with a further operating expenditure of £1.6million a year (USD 2.1million). The operating expenditure varies widely according to feedstock choice, availability, transport, and treatment.

4.2 Scale

Economy of scale is important for anaerobic digestion, given the costs involved. It’s especially important to be able to collect feedstock cheaply at scale and efficiently transport this to the digester. At the other end of the process, there obviously needs to be a use for the biogas. In many cases the offtaker is the business that installed the digester. In any case, digester operators need to have reassurance that the future supply of feedstock will be uninterrupted.

In an ideal world this would mean that digesters are located near large-scale feedstock sources, like energy crop plantations or clusters of dairy farms. But energy crops can take land out of food production. Many dairy farms in the UK are rural and so located away from biogas combined heat and power facilities or gas grid injection sites.

In addition, the UK government has only provided support for anaerobic digesters up to 250k MWh/year to “encourage geographical diversity”. While this has helped rapid uptake of anaerobic digestion in the 2010s, this may now limit future investments.

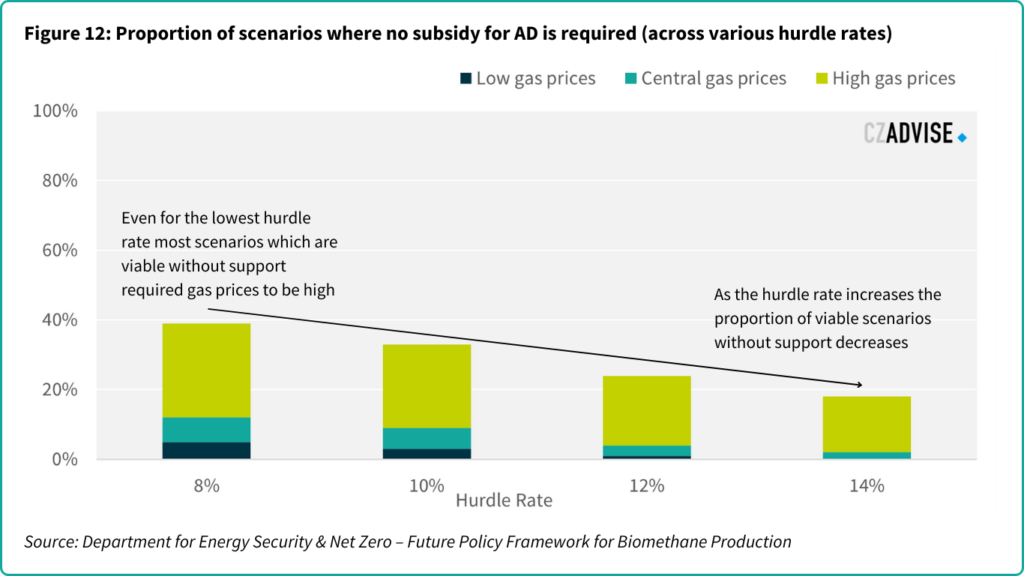

The UK government has modelled whether anaerobic digesters could be commercially viable without support under a range of scenarios. The modelling is shown in the chart below. For most scenarios they were not viable without support, even when high gas prices and low minimum expected rate of returns for projects were assumed. For example, with the lowest hurdle rate of 8%, less than 40% of scenarios are viable without any subsidy, this decreases to less than 20% of projects when the hurdle rate is 14%.

Small-scale anaerobic digesters which have been incentivised to date are typically on-farm plants which generate power and heat for on-site usage. Many existing anaerobic digesters produce biogas for power generation through combined heat and power plants. But the support for these plants via the Renewable Obligation and feed-in tariffs will soon start to expire. It’s not clear if these digesters will then be economically viable, but the government modelling suggests they will not be. Remember that there’s currently no government support on offer to upgrade existing biogas plants to biomethane.

4.3 Future Gas Demand

Many potential anaerobic digester operators are concerned about future UK demand for biogas and biomethane. The UK’s energy transition seems to be focused primarily on wind, solar and nuclear power, coupled with widespread electrification. This implies that overall natural gas usage may decline. Already, limits on gas grid capacity can make it difficult for some biomethane plants to inject into the grid at times, reducing revenues and increasing investment risk.

4.4 Other Revenue Streams

The solid waste product from an anaerobic digester is called digestate. It can be used as a fertiliser and so could potentially be a valuable source of revenue for plant operators. But it’s currently difficult to sell digestate as fertiliser in the UK as there are several environmental factors to consider:

- Possible ammonia release if improperly stored.

- Possible methane emissions during storage

- Risk to water courses during run-off.

Current permitting restrictions for digestate can lead to increased costs for testing, treatment and compliance. But if the digestate can’t be sold this can hit the digester’s profitability.

4.5 Permitting

Anaerobic digester operators must comply with the UK’s regulations on waste handling and environmental protection. It is classified as a chemical process and is permitted as such. Before construction, digesters require planning permission, which is determined by local authorities. Local residents’ concerns are part of the determination process, as are environmental assessments. These permits and controls ensure that anaerobic digesters are built correctly in a way that minimises risk to the environment, which is a core tenet of renewable energy. But they also add to the cost and time of building.

4.6 Looking to the Future

These are the main reasons why moderately sized British businesses like the dairy farm in Cornwall from our introduction don’t choose anaerobic digestion. They lack the scale to overcome the high costs involved and future revenues from biogas plants aren’t robust enough to justify the investment.

In the case of the farm in Cornwall, paying to mount solar panels on the cowshed roof was lower cost, faster, required less disruption and it was easier to model and understand the financial benefits. Consequently, just 9% of UK farmers currently use anaerobic digestion.

This is a shame because reducing carbon emissions from agriculture is going to be a core difficulty in reaching net zero and biogas/biomethane are mature technologies which can help abate these hard-to-reduce emissions.

Biogas only accounts for around 2% of the Europe’s energy output. This is such a small proportion of overall energy generation that it’s effectively ignored.

5. Biogas in Brazil

There are almost 900 operating biogas units in Brazil, of which around 80% use agricultural waste as a feedstock. Indeed, in recent years the agribusiness sector has been responsible for more than half of the new plants coming on stream. Most are small and in remote rural locations, where it’s hard to get constant electricity supply. Most biogas production is for on-site use: either at a farm or at an agricultural processor.

Some of the challenges faced by biogas expansion in Europe can be advantages in Brazil.

5.1 Support

Biogas’ main support in Brazil initially came from Resolution 482/2012 (Resolução ANEEL 482/2012), which establishes rules for the distribution of energy in sources of up to 5 MW, which further enables consumers to produce their own energy. In 2017, biogas was included in Brazil’s 10-Year National Energy Plan for the first time, and then in the National Biofuels Policy program, known as RenovaBio, launched in 2017.

Its main aim is to promote the expansion of biofuel production in the country by encouraging the gradual replacement of fossil fuel-based energy. RenovaBio sets decarbonisation targets for fuel distributors, creating demand for biofuels.

One tool of RenovaBio is tradable Decarbonisation Credits (CBIOs), which can be sold by biofuel producers and traders that meet their decarbonisation targets to those that need them, so acting as a source of revenue.

Biogas and biomethane also feature in the Future Fuel Bill, under which the National Energy Policy Council (CNPE) sets annual targets for the use of biomethane in the natural gas sector. The emissions reduction targets will start in January 2026, with an initial reduction goal of 1%, gradually increasing to 10%. Companies can meet these goals by directly using biomethane or purchasing Biomethane Origin Guarantee Certificates (CGOB), which will be freely traded between producers and importers.

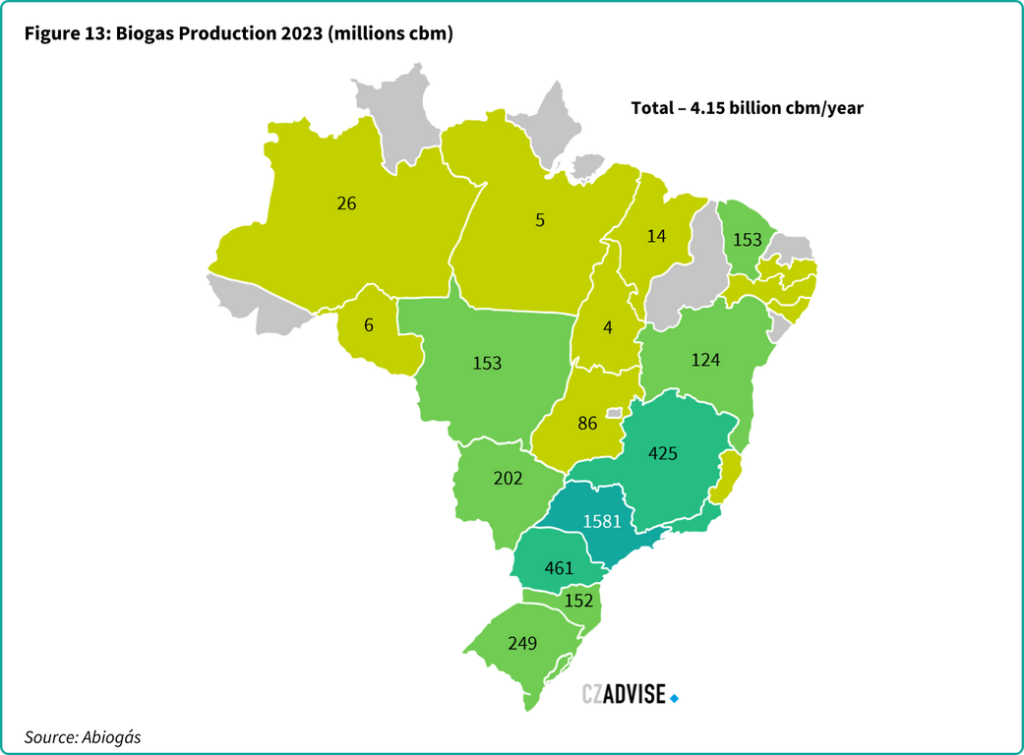

The support from the Brazilian government is therefore a mixture of mandate and incentive. It’s been sufficient to result in dramatic growth in the sector. From 1.3billion cbm in 2018 from 408 plants, Brazil can now produce more than 4billion cbm a year from over 900 plants.

5.2 Overcoming costs

Brazilian installation and operation costs for digesters vary widely according to feedstock and size. Upgrading from biogas to biomethane adds further expense, so its installation and operation costs are entirely different.

As an example, a hypothetical sugarcane mill crushing around 4.8million tonnes of cane a year to produce 149k cbm of ethanol (at an ethanol mix of 35%) should have approximately 1.6k cbm of vinasse available for anaerobic digestion. This is enough feedstock to support a plant producing around 10-12million cbm of biomethane each year plus 30,000-35,000 CBIOs. The capital expenditure to build a biomethane plant is around BRL 12-14/cbm, so we can assume this plant would cost around BRL 130million (USD 24million).

The capacity of this plant exceeds that of the one discussed in the UK. Comparing the costs—USD 22million in the UK and USD 24million in Brazil—this indicates that building a biogas plant in Brazil may be more economical. Additionally, economies of scale could also play a role in this difference.

This sort of project can be partly financed through the Brazilian Development Bank BNDES’ climate fund at low interest rates. The fund aims to assist projects which reduce greenhouse gas emissions. Ongoing maintenance costs are low at around BRL 90,000 per year.

One way which makes building a biogas plant more viable is to partner with an investor. This not only means the costs are shared it also means there is further access to resources such as technology and knowledge. An example of this is Albioma, a renewable energy producer, has partnered with Jalles, one of the largest sugar producers, in order to use the by-products from Jalles sugar production to produce renewable energy.

5.3 Overcoming scale

Biomethane production projects using vinasse from sugarcane are highly sensitive to scale. Once biomethane production reaches a certain level any further increase in production only leads to a marginal increase in capex and opex per unit of energy. This means there’s an incentive to make plants as large as the feedstock availability will allow, to improve project returns.

Most costs for biomethane plants are also fixed. The exceptions are energy and chemical inputs. This also benefits larger-scale projects. At today’s Brazilian natural gas prices, biomethane plants using vinasse as a feedstock are viable if they exceed 7.5million cbm in capacity.

Biomethane plants in Brazil benefit from a steady supply of agricultural feedstock due to the booming agricultural sector. Unlike in the UK, where farms are smaller and the aggregators are less significant, Brazil’s biomethane plants can collect crops and residues on a much larger scale. This makes it more feasible to leverage economies of scale to reduce costs in Brazil compared to the UK.

5.4 Demand for gas, power, hear and methane

Brazil is a vast country – 8.51million km2 – with many farms that are widely dispersed and decentralised, unlike the more compact landscape of the UK at 243,610 km2. The average size of farm in the UK is 85ha whereas in Brazil they are over 200ha, consequently the farms in Brazil are much more spread out. As a result, farms in Brazil have fewer options for accessing resources like gas, power, and heat from the grid, making biomethane production a more attractive option compared to farms in the UK. UK farms benefit from closer proximity to centralised energy sources, offering them a broader range of options.

Most Brazilian biogas units use the resulting heat and power on-site. This means that the plants are in control of their own demand.

Those that make biomethane can use it to generate heat or electricity for their own use or to sell it via power purchase agreements. It can also be sold as renewable natural gas replacing natural gas in industry and in agricultural machinery. For many agri-processors and farms, this latter use is the sweet spot. However, this may entail extra costs in converting engines to run on biomethane.

An example of this is Cocal in Brazil, the company we highlighted in our introduction. Production started in 2023 in partnership with GasBrasiliano to build a biogas plant with the potential for biomethane production. Scheduled for 2026, Cocal plans to invest BRL 216million (USD 40million) in a plant with a biomethane capacity of up to 60,000 cbm at the Paraguaçu Paulista unit.

Injecting biomethane into the national grid can be tricky as digesters need to be close to injection sites. There is also currently no differentiation between the biomethane and natural gas price, while the cost of natural gas production is lower.

Therefore, Brazil today hasn’t hit its biomethane potential. McKinsey estimates that Brazil makes almost all of its biomethane from urban waste and sewage, and almost none from agri-waste like sugar cane bagasse or animal slurry. Agriproducts comprise around 90% of possible biomethane feedstocks.

5.5 Other revenue

In the UK the digestate by-product from anaerobic digestion can be used as a biofertiliser, reducing the need for carbon-intensive mineral fertilisers.

In contrast, in Brazil, the treated vinasse – a by-product from the digestion process – has an organic loading rate of approximately 20% of the raw vinasse’s organic load but retains almost the same physical chemical composition. Given this, treated vinasse is used in agriculture, just as all raw vinasse is used in agriculture at plants that do not produce biogas. Biogas production plants at sugar and ethanol mills typically include agreements ensuring that the bio-digested vinasse is returned to the mill, rather than being sold as an additional revenue stream.

CBIOs can also be used as an additional source of revenue, CBIOs are part of Brazil’s RenovaBio program, which is designed to promote the production and use of biofuels, including biogas, by offering financial incentives through carbon credits. In order to receive the credit, the producer must undergo a certification process to quantify the carbon reduction achieved. Each CBIO corresponds to a tonne of carbon that is not released into the atmosphere. Following the example above 10-12million cbm of biomethane could receive 30,000-35,000 CBIOs.

5.6 Permitting

Building a biomethane plant in Brazil requires adherence to various legal requirements and licenses at the federal, state, and municipal levels. Both construction and biomethane production regulations must be considered, making it harder to initiate the project. Key requirements include environmental legislation, waste management regulations, and atmospheric emissions licenses, which vary based on the plant’s size and the types of emissions produced. For instance, specific regulations govern the authorisation for biofuel production and the facility’s operation.

Additionally, an Environmental Impact Assessment (EIA/RIMA) and public hearings may be necessary, depending on the project’s complexity. It’s also important to account for state-specific laws, which can impose restrictions on certain construction materials, such as banning the use of uncertified wood. While environmental legislation operates at the federal level, licenses are typically issued at the state level, meaning that additional state laws and regulations must also be followed.

6. Conclusion

Brazil’s biogas production has doubled in the past 5 years. We expect this growth to continue, driving capacity above the currently level of over 4billion cbm/year. This boom is driven by its large agribusiness and abundance of raw materials. To assist this the country has implemented several policies to encourage biogas production, such as Resolution 482/2012 and the RenovaBio initiative, which includes the introduction of CBIOs (carbon credits).

In contrast, the UK’s biogas industry is still growing, albeit at a slower pace. The UK also has a strong agricultural base but faces challenges such as stricter regulations and a smaller feedstock availability. The UK government supports biogas through schemes like the Renewable Heat Incentive (RHI), promoting the use of anaerobic digestion but without a direct equivalent to Brazil’s CBIOs.

While both countries recognise the potential of biogas, Brazil benefits from a more abundant resource base and a larger landmass with more remote rural farming businesses. Biogas really could become rural Brazil’s fuel of the future. We are ready to play our part to make this a reality.

Corporate advisers in agricultural and energy production

CZ Advise provides tailored consulting and corporate finance for agri-business and bioenergy supply chains.

Our consulting teams operate globally and offer a wide range of strategic advisory services to help companies successfully navigate the bioenergy sector. We specialise in market scoping, offering insights into emerging trends and opportunities across regions, as well as detailed cost analysis to help clients optimise operational efficiency and profitability. Additionally, we provide feedstock availability assessments and feasibility studies, ensuring that projects are not only economically viable but also sustainable in the long term. Our expertise in risk management and international partnerships enables us to help clients mitigate uncertainties while expanding into new markets with confidence.

James Brittain

Director, Head of Advisory

CZ Advise is the largest agri-focused financial advisor in Brazil and Southeast Asia and has advised on over USD 5.4 billion in debt and equity transactions, assisting companies in securing the financial backing they need for growth and innovation. Our corporate finance expertise spans fundraising, capital structuring, mergers and acquisitions, and project financing, ensuring that our clients have access to the best possible funding solutions to scale their operations in a competitive global market.

Luis Felipe Trinidade

Associate Director, Global Head of Corporate Finance

CZ’s trading teams can assist with the procurement, shipment, and stock management of ethanol and biomass, ensuring reliable supply chains for our clients. We also support ongoing feedstock visibility and storage solutions, enhancing transparency across the supply chain and helping businesses stay resilient in the face of fluctuating market conditions.

Get in touch with us to schedule a consultation.

Contact us

"*" indicates required fields